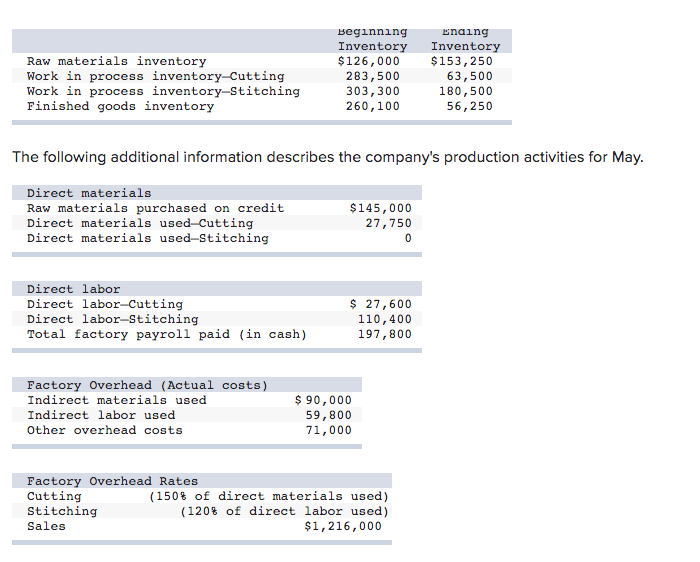

3 inventory accounts for a manufacturing business – In the realm of manufacturing, managing inventory is crucial for optimizing production, minimizing costs, and ensuring smooth operations. Understanding the three primary inventory accounts—Raw Materials Inventory, Work-in-Process Inventory, and Finished Goods Inventory—is essential for effective inventory management. These accounts track the flow of goods through the production process, providing valuable insights into the efficiency and profitability of manufacturing businesses.

As raw materials are transformed into finished products, these accounts capture the costs and quantities associated with each stage of production. By analyzing these accounts, manufacturers can identify areas for improvement, reduce waste, and enhance overall inventory management practices. This comprehensive overview delves into the characteristics, valuation methods, and significance of each inventory account, empowering manufacturing businesses to optimize their inventory strategies.

Inventory Accounts for Manufacturing: 3 Inventory Accounts For A Manufacturing Business

Inventory accounts play a crucial role in the efficient operation of a manufacturing business. They provide valuable insights into the flow of materials and products throughout the production process, helping businesses track costs, manage inventory levels, and optimize production schedules.

There are three main inventory accounts in a manufacturing business:

Raw Materials Inventory

Raw materials inventory represents the raw materials and components used in the production process. These materials are purchased from suppliers and stored until they are needed for production. The raw materials inventory account is debited when raw materials are purchased and credited when they are issued to production.

Work-in-Process Inventory

Work-in-process inventory represents the partially completed products that are still in the production process. This account includes the cost of raw materials, direct labor, and manufacturing overhead that have been incurred up to the point where the products are completed.

The work-in-process inventory account is debited as costs are incurred and credited when the products are completed and transferred to finished goods inventory.

Finished Goods Inventory

Finished goods inventory represents the completed products that are ready for sale to customers. This account is debited when products are completed and transferred from work-in-process inventory and credited when products are sold. The finished goods inventory account provides information about the quantity and value of products available for sale.

The relationship between these three inventory accounts can be summarized as follows:

- Raw materials inventory is transformed into work-in-process inventory as production begins.

- Work-in-process inventory is transformed into finished goods inventory as production is completed.

- Finished goods inventory is sold to customers, generating revenue for the business.

Raw Materials Inventory

Raw materials are the basic components used in the production of finished goods. They are typically purchased from suppliers and stored in inventory until they are needed for production.

Raw materials inventory is accounted for using the same methods as other inventory accounts. The most common methods are first-in, first-out (FIFO), last-in, first-out (LIFO), and weighted average.

Valuation Methods

- FIFOassumes that the first raw materials purchased are the first to be used in production. This method results in the highest cost of goods sold (COGS) during periods of rising prices.

- LIFOassumes that the last raw materials purchased are the first to be used in production. This method results in the lowest COGS during periods of rising prices.

- Weighted averageassumes that all raw materials purchased are used evenly throughout the production period. This method results in a COGS that is somewhere between FIFO and LIFO.

Impact on Production Costs

The choice of raw materials inventory valuation method can have a significant impact on production costs. FIFO results in the highest COGS during periods of rising prices, while LIFO results in the lowest COGS. Weighted average falls somewhere in between.

Work-in-Process Inventory

Work-in-process inventory (WIP) refers to the partially completed goods that are still in the production process and have not yet reached their finished state. It represents the costs incurred up to the point of the inventory’s current stage of completion.

WIP is a critical component of manufacturing operations, as it reflects the progress of production and the efficiency of the manufacturing process.

The valuation of WIP depends on the stage of production. For example, raw materials that have undergone some processing but are not yet fully transformed into finished goods would be valued at a higher cost than raw materials that have not yet been processed.

Similarly, partially assembled components would be valued at a higher cost than raw materials, as they represent a more advanced stage of production.

Stages of Production

- Raw material stage: This stage involves the acquisition and storage of raw materials, which are the basic components used in the production process.

- Work-in-process stage: This stage involves the conversion of raw materials into finished goods through various production processes.

- Finished goods stage: This stage involves the completion of the production process and the storage of finished goods, which are ready for sale to customers.

Management and Control of WIP

Effective management and control of WIP is crucial for maintaining efficient production operations. Some common methods include:

- Just-in-time (JIT) inventory system:JIT aims to minimize WIP by producing goods only when they are needed, reducing the amount of inventory held on hand.

- Kanban system:Kanban is a visual system that uses cards to track the flow of WIP through the production process, ensuring that each stage of production has the necessary materials and components.

- Material requirements planning (MRP):MRP is a software-based system that helps manufacturers plan and manage the flow of materials and components through the production process, ensuring that the right materials are available at the right time.

Finished Goods Inventory

Finished goods inventory refers to products that have completed all production processes and are ready for sale to customers. They represent the final stage of the manufacturing cycle and play a crucial role in determining a company’s financial performance.

Finished goods inventory is accounted for as an asset on the company’s balance sheet. It is valued using various methods, such as FIFO (first-in, first-out), LIFO (last-in, first-out), and weighted average. The choice of valuation method can significantly impact the company’s financial statements.

Impact on Financial Performance

Finished goods inventory has a direct impact on a company’s financial performance in several ways:

- Cost of Goods Sold:The value of finished goods inventory is used to calculate the cost of goods sold, which is a major expense on the income statement.

- Gross Profit:Finished goods inventory is a component of gross profit, which is calculated as sales revenue minus the cost of goods sold.

- Current Ratio:Finished goods inventory is included in the calculation of the current ratio, which measures a company’s ability to meet its short-term obligations.

- Inventory Turnover:Inventory turnover measures how efficiently a company is managing its inventory. A higher inventory turnover rate indicates that the company is selling its finished goods quickly and not holding excessive inventory.

Inventory Management Techniques

Inventory management techniques play a crucial role in manufacturing businesses, enabling them to optimize inventory levels, reduce costs, and enhance profitability. These techniques encompass a range of approaches, each with its unique benefits and limitations.

Effective inventory management techniques can lead to significant improvements in efficiency and profitability. By minimizing excess inventory, businesses can reduce carrying costs, such as storage and insurance expenses. Additionally, optimized inventory levels can prevent stockouts, ensuring uninterrupted production and customer satisfaction.

Just-in-Time (JIT) Inventory

JIT is a popular inventory management technique that aims to minimize inventory levels by receiving materials and components only when they are needed for production. This approach reduces storage costs and the risk of obsolescence. However, JIT requires close coordination with suppliers and can be challenging to implement in industries with long lead times.

Economic Order Quantity (EOQ)

EOQ is a mathematical formula used to determine the optimal order quantity for inventory items. It considers factors such as demand, ordering costs, and holding costs to minimize the total inventory costs. EOQ helps businesses avoid both overstocking and understocking, ensuring optimal inventory levels.

Safety Stock

Safety stock is an additional inventory level maintained to buffer against unexpected fluctuations in demand or supply. It protects businesses from stockouts and ensures uninterrupted production. However, holding safety stock incurs additional carrying costs, so it is essential to determine the appropriate safety stock level.

First-In, First-Out (FIFO)

FIFO is an inventory valuation method that assumes that the oldest inventory items are sold first. This method helps ensure that inventory is fresh and prevents the accumulation of obsolete items. However, FIFO can result in higher inventory costs during periods of rising prices.

Last-In, First-Out (LIFO)

LIFO is an inventory valuation method that assumes that the most recently acquired inventory items are sold first. This method can result in lower inventory costs during periods of rising prices but may lead to the accumulation of older inventory items.

Inventory Valuation Methods

Inventory valuation methods are used to determine the value of inventory on a company’s financial statements. There are several different methods that can be used, each with its own advantages and disadvantages.

The most common inventory valuation methods are:

- First-in, first-out (FIFO)

- Last-in, first-out (LIFO)

- Weighted average cost

First-in, First-out (FIFO)

FIFO assumes that the first items purchased are the first items sold. This means that the cost of goods sold is based on the cost of the oldest inventory on hand. FIFO can result in higher cost of goods sold and lower net income in periods of rising prices.

Last-in, First-out (LIFO)

LIFO assumes that the last items purchased are the first items sold. This means that the cost of goods sold is based on the cost of the most recent inventory on hand. LIFO can result in lower cost of goods sold and higher net income in periods of rising prices.

Weighted Average Cost

Weighted average cost assumes that all units of inventory are purchased at the same cost. This means that the cost of goods sold is based on the average cost of all inventory on hand. Weighted average cost can result in a more stable cost of goods sold and net income than FIFO or LIFO.

Impact of Inventory Valuation Methods on Financial Statements

The choice of inventory valuation method can have a significant impact on a company’s financial statements. FIFO can result in higher cost of goods sold and lower net income in periods of rising prices. LIFO can result in lower cost of goods sold and higher net income in periods of rising prices.

Weighted average cost can result in a more stable cost of goods sold and net income than FIFO or LIFO.

Inventory Control Systems

Inventory control systems are essential for manufacturing businesses to manage their inventory levels effectively. These systems help businesses track inventory items, monitor inventory levels, and optimize inventory replenishment. There are several different inventory control systems used in manufacturing businesses, each with its own key features and benefits.

Periodic Inventory System

The periodic inventory system is a simple and straightforward inventory control system that involves counting inventory items at regular intervals, such as monthly or quarterly. This system is relatively easy to implement and manage, but it can be time-consuming and may not provide real-time visibility into inventory levels.

Perpetual Inventory System, 3 inventory accounts for a manufacturing business

The perpetual inventory system is a more sophisticated inventory control system that tracks inventory items in real-time. This system uses a computerized database to record every inventory transaction, such as receipts, shipments, and adjustments. The perpetual inventory system provides real-time visibility into inventory levels and can help businesses identify trends and patterns in inventory usage.

Just-in-Time (JIT) Inventory System

The just-in-time (JIT) inventory system is a lean inventory control system that aims to minimize inventory levels and reduce waste. This system involves producing only the inventory that is needed, when it is needed. The JIT inventory system can help businesses reduce inventory carrying costs and improve cash flow.

Inventory Optimization

Inventory optimization is a critical aspect of inventory management that involves determining the optimal levels of inventory to hold to meet customer demand while minimizing costs. It plays a significant role in manufacturing businesses, where managing inventory levels effectively can lead to substantial cost savings and improved efficiency.Inventory optimization techniques aim to strike a balance between holding too much inventory, which ties up capital and incurs storage and handling costs, and holding too little inventory, which can lead to stockouts and lost sales.

By optimizing inventory levels, businesses can reduce their carrying costs, improve customer service, and increase overall profitability.

Techniques for Inventory Optimization

Various techniques are employed to optimize inventory levels, including:

Safety Stock Management

Maintaining a buffer stock to mitigate risks associated with demand variability and supply chain disruptions.

Just-in-Time (JIT) Inventory

Minimizing inventory levels by receiving materials and components only when they are needed for production.

Economic Order Quantity (EOQ)

Determining the optimal quantity to order at a time to minimize total inventory costs.

Vendor-Managed Inventory (VMI)

Allowing suppliers to manage inventory levels based on demand forecasts.

Demand Forecasting

Predicting future demand to ensure adequate inventory levels and avoid stockouts.

Inventory Tracking Systems

Using technology to monitor inventory levels in real-time and identify trends and patterns.

Benefits of Inventory Optimization

Effective inventory optimization can lead to several benefits for manufacturing businesses, including:

Reduced Inventory Costs

Lower carrying costs, storage costs, and handling expenses.

Improved Customer Service

Reduced stockouts and faster delivery times.

Increased Production Efficiency

Optimized inventory levels support smooth production flow and reduce downtime.

Enhanced Profitability

Overall cost savings and improved efficiency contribute to increased profitability.

Improved Cash Flow

Reduced inventory levels free up capital for other business operations.

Final Review

In conclusion, the three inventory accounts—Raw Materials Inventory, Work-in-Process Inventory, and Finished Goods Inventory—form the backbone of inventory management in manufacturing businesses. Understanding the nuances of each account enables manufacturers to effectively track inventory levels, control costs, and make informed decisions that drive operational efficiency and profitability.

By leveraging inventory management techniques, valuation methods, and control systems, manufacturing businesses can optimize their inventory strategies, minimize waste, and maximize the value of their inventory investments.

FAQ Resource

What is the purpose of Raw Materials Inventory?

Raw Materials Inventory tracks the raw materials used in the production process, including their quantities and costs.

How is Work-in-Process Inventory valued?

Work-in-Process Inventory can be valued using various methods, such as FIFO (First-In, First-Out), LIFO (Last-In, First-Out), or weighted average.

What is the significance of Finished Goods Inventory?

Finished Goods Inventory represents the completed products ready for sale, providing insights into production efficiency and customer demand.